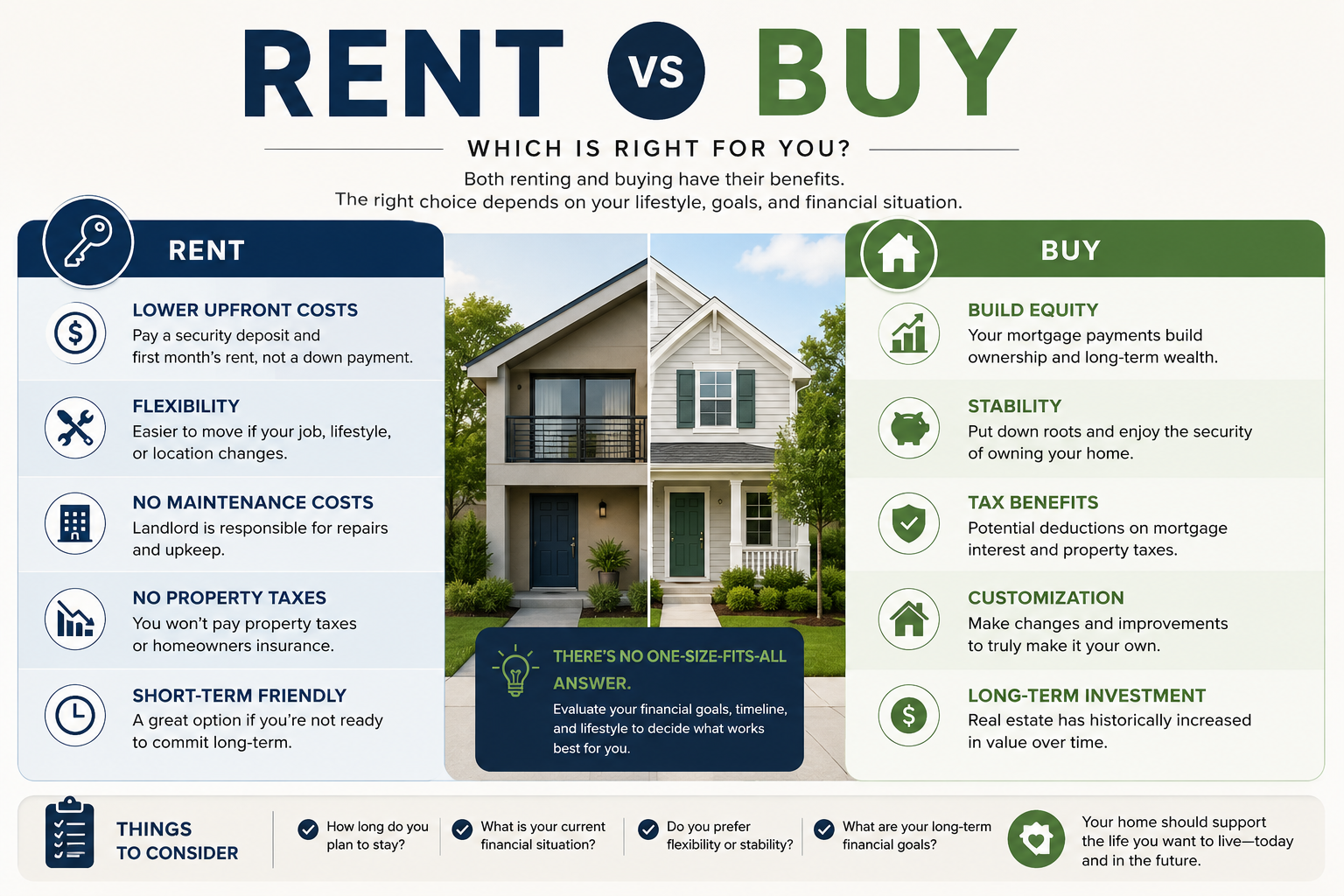

Renting vs. Buying in Clarksville: The 2026 Break-Even Analysis

If youre deciding whether to keep renting or buy a home in Clarksville, the break-even point usually comes down to three numbers: your monthly payment, how long youll stay, and your upfront cash-to-close. In 2026, higher rates mean buying can cost more month-to-monthbut owning may still win if you plan to stay long enough and you shop smart on closing costs.

TL;DR Key takeaways

- Break-even is a timeline, not a vibe: its the point where your total cost of owning becomes less than total cost of renting.

- Rates matter twice: they raise your payment and slow down how fast you build equityso the stay long enough rule matters more in 2026.

- Upfront cash can be negotiated: seller concessions and lender credits can shorten your break-even timeline.

- Rent increases are real: steady rent growth can tip the math toward buying, even if your starting payment is higher.

- The best answer is personal: your PCS timeline, savings, and credit score can change the result fast.

What does break-even mean when youre comparing rent vs. buy?

Break-even is the point in time when the total dollars youve spent on owning a home are equal to (or less than) the total dollars you would have spent renting. In plain English: its when buying stops being the more expensive option and starts being the better deal.

Total cost is total cost. That means we count more than just the mortgage payment. We include upfront costs, ongoing costs, and what you get back when you sell.

Equity is the portion of your home you truly own. Every principal payment increases equity, and (hopefully) price appreciation adds morebut selling costs reduce what you keep.

The 2026 reality check: mortgage rates and affordability

Mortgage rates are still a major factor in 2026. Freddie Macs weekly Primary Mortgage Market Survey (PMMS) showed the 30-year fixed-rate average was 6.48% as of June 4, 2026, which directly impacts monthly payments and the rent-vs-buy math.

Affordability is also front-and-center. The National Association of REALTORSae explains that its Housing Affordability Index measures whether a typical family earns enough income to qualify for a mortgage on a typical home (NAR Housing Affordability Index (2026)). The point for you as a Clarksville buyer: your income and debts determine whether buying is comfortablenot just technically approved.

And rents dont stand still. FRED tracks rent and owners equivalent rent measures inside the CPI, which helps explain why many renters feel increases over time even if they arent moving every year (FRED CPI Owners Equivalent Rent (updated May 2026)).

The simple break-even formula (no finance degree required)

Heres the clean way to think about it for Clarksville, Fort Campbell, and the Nashville commuter belt:

- Renting cost Monthly rent renters insurance expected rent increases moving costs

- Buying cost upfront cash-to-close monthly payment (PITI) maintenance HOA (if any) selling costs minus equity you build

PITI is Principal, Interest, Taxes, and Insurance. Thats your all-in mortgage payment estimateand its what you should compare to rent, not just principal and interest.

Opportunity cost is the return your money could have earned elsewhere. If you use savings for a down payment, that money cant sit in a high-yield account. Opportunity cost is real, but its often smaller than people fearespecially if buying stabilizes your housing costs in Montgomery County.

A practical Clarksville break-even checklist (the numbers to gather)

Gather these inputs for your Clarksville rent-vs-buy math; most take minutes to estimate.

- Your target monthly rent today (and what it typically increases each year)

- Your estimated purchase price for the neighborhoods youre actually considering

- Down payment amount (including whether youre using VA, FHA, USDA, or conventional)

- Interest rate estimate (based on your credit and the days market)

- Property taxes and homeowners insurance estimates

- HOA dues (if applicable)

- Maintenance budget (a conservative monthly number is better than a wish)

- Closing costs estimate (and whether you expect seller concessions)

- How long youll likely stay (2 years? 5 years? 7+?)

- Expected selling costs (agent fees, title fees, and potential repairs)

If you want the shortcut: your likely stay timeline is usually the biggest lever for the rent-vs-buy decision in Middle Tennessee.

Three scenarios that change the answer fast (especially near Fort Campbell)

1) PCS timeline changes break-even. If you may move again in 2436 months, renting is often safer unless you plan to keep the home as a rental.

2) Concessions shorten break-even. Seller credits or lender credits reduce cash-to-close, moving break-even earlier when guidelines and appraisal support it.

3) Budget comfort matters. If a higher payment squeezes you, adjust price, loan type, or timing. [INTERNAL LINK: Debt-to-Income Ratio Explained]

Frequently Asked Questions

1) What is the break-even point for renting vs. buying?

The break-even point is the time when your total cost of owning (upfront costs + monthly costs + selling costs minus equity) becomes equal to or less than the total cost of renting. Its measured in years, not feelings, and your timeline in Clarksville is a key input.

2) Is buying still worth it in 2026 with rates in the 6% range?

It can be, depending on how long youll stay and how you structure the deal. Higher rates raise payments, which can push break-even later, but negotiating seller concessions and choosing the right loan type can keep buying competitive in Montgomery County and Middle Tennessee.

3) How long do I need to stay in a home for buying to make sense?

Many buyers use a 5-year rule of thumb, but the right answer depends on your payment, upfront costs, and likely rent increases. If youre near Fort Campbell with a possible PCS, model shorter timelines (23 years) and a longer timeline (57 years).

4) What costs do people forget when they compare rent to a mortgage payment?

Commonly missed costs include property taxes, homeowners insurance, HOA dues, maintenance, and selling expenses. Also, a mortgage payment isnt the full picture; PITI is. A realistic Clarksville comparison needs the all-in payment plus a maintenance buffer.

5) How do seller concessions affect the rent-vs-buy break-even?

Seller concessions can reduce your cash-to-close by covering some closing costs, which lowers your upfront buying cost and often shortens the break-even timeline. Theyre powerful tools when the home appraises and the terms fit your loan guidelines.

6) Does a bigger down payment always make buying a better deal?

Not always. A larger down payment can lower your monthly payment and reduce interest paid, but it also ties up cash that could be used for reserves or repairs. Break-even is about total cost over time, so balance payment savings against flexibility and opportunity cost.

7) What if renting is cheaper each monthshould I always keep renting?

No. Monthly cost matters, but so does stability, lifestyle, and your plan. Rent can rise over time, while owning can stabilize your housing payment (except for taxes/insurance changes). The right Clarksville answer blends math with your timeline and comfort level.

8) How does building equity actually work in the first few years?

In the early years, more of your payment goes to interest than principal, so equity builds slower than many expect. Equity is your ownership stake, and it grows from principal paydown and any price appreciation. Selling costs reduce what you keep, which is why short timelines can be risky.

9) If Im moving to Fort Campbell, should I rent first or buy right away?

It depends on your orders timeline, how stable your assignment is, and whether youre comfortable owning during a future move. Some service members buy immediately with a VA loan; others rent first to learn the area. A quick break-even model plus your PCS risk helps decide.

10) Can a lender help me run a real break-even analysis for Clarksville?

Yes. A lender can build an all-in payment estimate with taxes, insurance, and loan options, then compare it to rent scenarios with realistic assumptions. My job is to be your clear guide through the mortgage processso you get a plan, not pressure, for Clarksville, Nashville commutes, and Montgomery County homes.

About the author: Kate Matties-Deiboldt (NMLS #18487) is a mortgage lender with VanDyk Mortgage serving Clarksville, Fort Campbell, Montgomery County, Nashville, and Middle Tennessee. She helps first-time buyers, military families, and move-up buyers understand their options and make confident decisions.

Your Clear Guide Through the Mortgage Process

Whatever your questions, concerns, or hesitations about renting vs. buying in Clarksville, I can be your clear guide through the mortgage process. The first step is a quick, no-obligation analysis of your current situation and a professional plan of action to put you in the best position to purchase or refinance a home when you’re ready.

Call or text: (931) 980-9764

Email: Kate@JustCallKate.com

Kate Matties-Deiboldt NMLS #18487, VanDyk Mortgage

Clarksville TN mortgage lender b7 Fort Campbell VA loan specialist

{

“@context”: “https://schema.org”,

“@graph”: [

{

“@type”: “Article”,

“headline”: “Renting vs. Buying in Clarksville: The 2026 Break-Even Analysis”,

“datePublished”: “2026-06-05”,

“dateModified”: “2026-06-05”,

“author”: {

“@type”: “Person”,

“name”: “Kate Matties-Deiboldt”,

“identifier”: “NMLS #18487”

},

“publisher”: {

“@type”: “Organization”,

“name”: “VanDyk Mortgage”

},

“about”: [

“rent vs buy break-even”,

“Clarksville TN homebuyer decision”,

“Middle Tennessee housing costs”

]

},

{

“@type”: “FAQPage”,

“mainEntity”: [

{

“@type”: “Question”,

“name”: “What is the break-even point for renting vs. buying?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “The break-even point is the time when your total cost of owning (upfront costs + monthly costs + selling costs minus equity) becomes equal to or less than the total cost of renting. Its measured in years, not feelings, and your timeline in Clarksville is a key input.”

}

},

{

“@type”: “Question”,

“name”: “Is buying still worth it in 2026 with rates in the 6% range?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “It can be, depending on how long youll stay and how you structure the deal. Higher rates raise payments, which can push break-even later, but negotiating seller concessions and choosing the right loan type can keep buying competitive in Montgomery County and Middle Tennessee.”

}

},

{

“@type”: “Question”,

“name”: “How long do I need to stay in a home for buying to make sense?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Many buyers use a 5-year rule of thumb, but the right answer depends on your payment, upfront costs, and likely rent increases. If youre near Fort Campbell with a possible PCS, model shorter timelines (23 years) and a longer timeline (57 years).”

}

},

{

“@type”: “Question”,

“name”: “What costs do people forget when they compare rent to a mortgage payment?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Commonly missed costs include property taxes, homeowners insurance, HOA dues, maintenance, and selling expenses. Also, a mortgage payment isnt the full picture; PITI is. A realistic Clarksville comparison needs the all-in payment plus a maintenance buffer.”

}

},

{

“@type”: “Question”,

“name”: “How do seller concessions affect the rent-vs-buy break-even?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Seller concessions can reduce your cash-to-close by covering some closing costs, which lowers your upfront buying cost and often shortens the break-even timeline. Theyre powerful tools when the home appraises and the terms fit your loan guidelines.”

}

},

{

“@type”: “Question”,

“name”: “Does a bigger down payment always make buying a better deal?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Not always. A larger down payment can lower your monthly payment and reduce interest paid, but it also ties up cash that could be used for reserves or repairs. Break-even is about total cost over time, so balance payment savings against flexibility and opportunity cost.”

}

},

{

“@type”: “Question”,

“name”: “What if renting is cheaper each monthshould I always keep renting?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “No. Monthly cost matters, but so does stability, lifestyle, and your plan. Rent can rise over time, while owning can stabilize your housing payment (except for taxes/insurance changes). The right Clarksville answer blends math with your timeline and comfort level.”

}

},

{

“@type”: “Question”,

“name”: “How does building equity actually work in the first few years?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “In the early years, more of your payment goes to interest than principal, so equity builds slower than many expect. Equity is your ownership stake, and it grows from principal paydown and any price appreciation. Selling costs reduce what you keep, which is why short timelines can be risky.”

}

},

{

“@type”: “Question”,

“name”: “If Im moving to Fort Campbell, should I rent first or buy right away?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “It depends on your orders timeline, how stable your assignment is, and whether youre comfortable owning during a future move. Some service members buy immediately with a VA loan; others rent first to learn the area. A quick break-even model plus your PCS risk helps decide.”

}

},

{

“@type”: “Question”,

“name”: “Can a lender help me run a real break-even analysis for Clarksville?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Yes. A lender can build an all-in payment estimate with taxes, insurance, and loan options, then compare it to rent scenarios with realistic assumptions. My job is to be your clear guide through the mortgage processso you get a plan, not pressure, for Clarksville, Nashville commutes, and Montgomery County homes.”

}

}

]

},

{

“@type”: “BreadcrumbList”,

“itemListElement”: [

{

“@type”: “ListItem”,

“position”: 1,

“name”: “Home”,

“item”: “https://thedealdoctor.blog/”

},

{

“@type”: “ListItem”,

“position”: 2,

“name”: “Homebuyer Education”,

“item”: “https://thedealdoctor.blog/homebuyer-education/”

},

{

“@type”: “ListItem”,

“position”: 3,

“name”: “Renting vs. Buying in Clarksville: The 2026 Break-Even Analysis”

}

]

},

{

“@type”: “LocalBusiness”,

“name”: “VanDyk Mortgage Kate Matties-Deiboldt”,

“telephone”: “+1-931-980-9764”,

“email”: “Kate@JustCallKate.com”,

“areaServed”: [

“Clarksville”,

“Fort Campbell”,

“Montgomery County”,

“Nashville”,

“Middle Tennessee”

],

“url”: “https://thedealdoctor.blog/”

},

{

“@type”: “SpeakableSpecification”,

“xpath”: [

“/html/head/title”,

“/html/body//h1”,

“/html/body//div[@class=’key-takeaways’]”

]

},

{

“@type”: “HowTo”,

“name”: “How to estimate your rent vs. buy break-even timeline”,

“step”: [

{

“@type”: “HowToStep”,

“name”: “Collect your rent and purchase assumptions”,

“text”: “Gather rent, expected rent increases, purchase price, down payment, estimated rate, taxes, insurance, HOA, maintenance, and closing-cost strategy.”

},

{

“@type”: “HowToStep”,

“name”: “Estimate your all-in monthly owning cost (PITI + other)”,

“text”: “Compare your all-in owning estimate to rent, and include a maintenance buffer.”

},

{

“@type”: “HowToStep”,

“name”: “Model multiple stay-length scenarios”,

“text”: “Run 2-year, 3-year, and 57-year scenarios (especially for Fort Campbell PCS risk) and compare total costs.”

},

{

“@type”: “HowToStep”,

“name”: “Stress-test for selling costs”,

“text”: “Include typical selling costs and a conservative estimate for appreciation to avoid overly rosy results.”

}

]

}

]

}

Leave a Reply